Raj Shah, Director and Principal of Blue Wealth Capital talks about the important role life (or 'human') insurance plays.

In last month’s article I wrote about the importance of business succession planning and ensuring the wishes of shareholders are properly documented.

Life insurance (I prefer to call it human insurance) can play an important role when it comes to underpinning your wealth/succession planning and if you own your own business there can be a highly tax efficient way of organising this through your company.

Case Study

Sarah Owens is a founder and managing director of a user experience design consultancy in South Yorkshire. After leaving her previous employer and setting up her own company, Sarah has lost her death-in-service benefit. Her high quality financial planner suggests she purchases life insurance through her company, and after comparing relevant life insurance to standard life insurance, it appears relevant life insurance is a more beneficial option for Sarah.

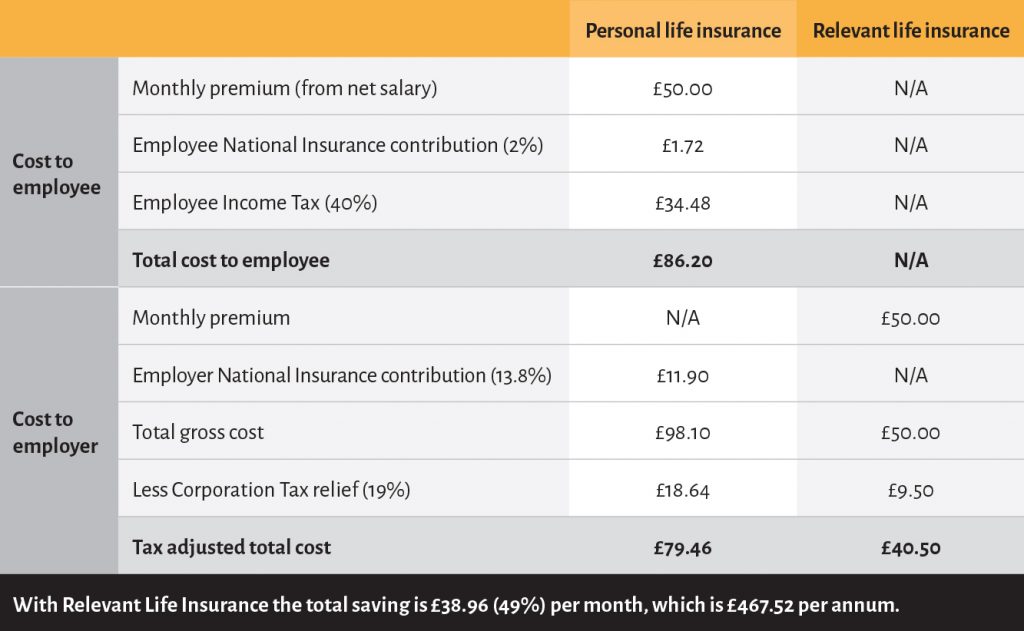

Example: Sarah would like £1 million of cover. She is a higher rate taxpayer (40%) and pays National Insurance at 2% on the top end of her income. The company pays National Insurance at 13.8% (this assumes that the employee is not contracted out of the Additional State Pension). Corporation Tax is calculated at a rate of 19% since April 2017. This illustration shows the difference in the gross cost of an employer providing life cover for an employee through a Relevant Life insurance policy compared to a personal policy Sarah could take out herself.

Any tax and National Insurance is calculated based on the cost to the employee, i.e. how much it would cost an employee in total to pay a premium taking account of Income Tax, National Insurance and the premium. For example, in order for Sarah to be able to pay a premium of £50.00, she would need to earn £86.20 on which she would have to pay Income Tax of £34.48 and National Insurance of £1.72.

To get the total net cost to the employer you would need to add the employer’s National Insurance contribution costs and then deduct Corporation Tax Relief. The information provided in these examples is for illustrative purposes only; the examples are purely fictitious and individual circumstances should be thoroughly assessed to calculate potential savings to the employer/employee.

The illustrations are based on my understanding of current law and HM Revenue & Customs practice as at October 2019 which may change in the future. Tax calculations are based on 2019/20 tax rates and may also change in the future. The calculations assume that the same rate of Income Tax/National Insurance applies to the whole of the premium or sums used to fund the premium.

Consulting a high quality financial planner could not only help you increase your wealth, but could save you a few precious pounds in human insurance premiums.

Raj Shah is founder of Blue Wealth capital and has been shortlisted for Financial Planner of the Year and Investment Adviser of the Year.